Source: Cisco

Last week Cisco (NASDAQ: CSCO) reported its third quarter fiscal year 2017 financials for the period ended April 29, 2017. The company had $11.9 billion in revenue, a 1 percent decrease year over year. Recurring revenue represented 31 percent of the total, a 2 percent increase year over year. The company also reported GAAP net income of $2.5 billion, or GAAP diluted earnings per share of $0.50.

Other highlights for the quarter include:

- Product revenue was flat and service revenue was down 2 percent.

- Deferred revenue was $17.3 billion, a 13 percent increase, with deferred product revenue up 26 percent, driven largely by subscriptions.

- Total gross margin was 63 percent, and product gross margin was 61.7 percent (GAAP).

- Operating expenses were $4.3 billion, an 8 percent decrease year over year (GAAP).

- Operating income was $3.2 billion, a 6 percent increase year over year (GAAP).

“We delivered a solid quarter with total revenue of $11.9 billion and non-GAAP earnings per share of $0.60. We had strong margins yet again and great operating cash flow, up 10 percent. We are managing the business well through a multiyear transformation of the company, while remaining focused on delivering customers unparalleled value through highly secure, software-defined, automated and intelligent infrastructure,” said CEO Chuck Robbins on the earnings call.

“We are on a journey, which, as we’ve consistently stated, will take a number of years, but we are pleased with the progress we’re making. As our customers add billions of new connections in the years ahead, the network will become more critical than ever,” Robbins added. “They will be looking for intelligent networks that deliver automation, security and analytics that help them derive meaningful business value from these connections. These will be delivered through a combination of new platforms as well as software and subscription-based services, which we’ve been focused on accelerating over the last 18 months.”

In its earnings report, Cisco announced that its $3.7 billion acquisition of AppDynamics was completed in the third quarter. The company also reiterated recent announcements of pending acquisitions, including Viptela, Inc., a software-defined wide area network company, the Advanced Analytics team and associated advanced analytics intellectual property by Saggezza, and MindMeld, Inc., an artificial intelligence company. The acquisitions for Viptela, Advanced Analytics and MindMeld are expected to close in 2017.

“These acquisitions support our goal of offering customers extraordinary value through a combination of organic and inorganic innovation, and they are aligned to our strategy of investing to drive long-term growth and helping us transition to more recurring software and subscription revenue. We will continue to deploy our capital resources to give us first-mover advantage as we extend our technology portfolio,” said Robbins.

For the fourth quarter, Cisco estimates that revenue will be down 4 percent to 6 percent year over year, and GAAP earnings per share will range between $0.46 and $0.51.

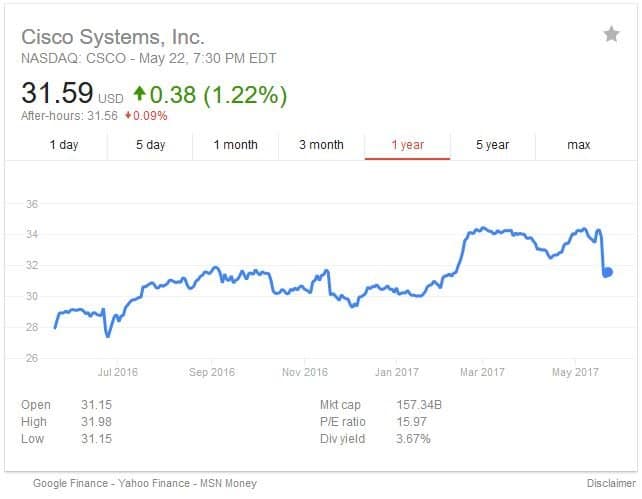

Investors were not impressed, either with the quarter’s financials or with the guidance that the company expects revenue to be down in the next quarter. On May 16, the day before financials were released, the stock price per share was $34.30. On May 17, the day financials were released, stock dropped to $33.82 per share. As of 7:30 PM EDT on May 22, stock was $31.59 per share in after-hours trading. While the drop is concerning, stock is still valued above where it was this time last year. On May 23, 2016, Cisco was valued at $27.94 per share.

Source: Google Finance – Yahoo Finance – MSN Money

Insider Take:

Robbins’ remarks reiterate the company’s shift toward a subscription-based SaaS model. Wall Street analysts like The Street have speculated that Cisco’s financials indicate that the company isn’t moving fast enough to make up to offset challenges and its recent acquisitions perhaps could help the company get up to speed faster than it can on its own. The company’s performance in the next quarter will be telling.